Ever wonder what life will be like after you stop working? Often, what retirement will look like depends on how you prepare before you retire. Whether retirement is a year away or 25 years, learn what you need to know now for retirement later.

Costco 401(k) Retirement Plan: The annual company contribution helps you grow your savings

Costco invests in your future with both matching and annual company contributions to your Costco 401(k) Retirement Plan account. Employees in Puerto Rico have the Costco Puerto Rico Retirement Plan.

Eligibility: Once an employee has completed a year of service, they’ll be entered into the company contribution portion of the plan beginning the first day of the month after their anniversary date.

Annual company contribution: Costco contributes a percentage of eligible earnings paid from the entry date – regular pay, overtime, vacation pay, holiday pay, sick pay, paid time off and extra checks – to your 401(k) account*, even if you don’t make any contributions of your own.

The contribution starts at 4% for an employee’s first few years, and increases as your years of service increase, capping at 9% after 25 years.

Matching company contribution: The company also matches 50% of your own contributions, up to $500 a year.

Best of all – these contributions belong to you with immediate 100% vesting.

To check your account balance, set up automatic payroll deductions, adjust your investment mix and much more, go to RPS.TRowePrice.com. You’ll also find financial tools and resources, including an Education Library, Retirement Income Planner and calculators:

Paycheck Impact Calculator

Contribution Maximizer

College Planning Calculator

Roth Comparison Calculator

Social Security Calculator and more

2024 Annual company contribution: Costco contributed nearly $616 million to employee retirement accounts in 2025 for the 2024 annual company contribution. If you missed the letter Costco sent noting this year’s contribution amount, see your quarterly statement from T. Rowe Price.

Years of Service

Company Contribution

Average Contribution Per Year

1-3 years

4%

$1,371

4-9 years

5%

$2,996

10-14 years

6%

$4,198

15-19 years

7%

$4,994

20-24 years

8%

$5,897

25+ years

9%

$7,147

*Employees at union warehouses should consult their collective bargaining agreement for more information about Costco’s contributions to their 401(k) plan.

Purchase company stock and become a shareholder in the company

The Employee Stock Purchase Plan (ESPP) with UBS lets you purchase Costco stock through payroll deductions. You choose the amount you’d like to invest each pay period. Fees and commissions for these purchases are fully paid by Costco. To learn more, visit Costcobenefits.com > Financial Wellbeing > Employee Stock Purchase Plan (ESPP).

Get familiar with Medicare — know your health coverage options before and after 65

While Medicare is available beginning at age 65, if you retire before age 65, you’ll need health coverage to fill the gap. You can explore coverage options available at HealthCare.gov, or you can contact the Benefits Department at 800-284-4882 to learn more about your retirement health plan options.

Do you or a family member have questions about Medicare, Medicare Advantage or Supplemental plans? Get answers to your questions. SGIA Medicare Consulting offers one-on-one support to help you find the plan that fits your needs. This service is available at no cost to all Costco employees and their families, including parents.

To connect with a Medicare expert, call 888-821-6486 or learn more at sgiamedicare.com/costco.

Dealing with money and finances can be overwhelming. But small changes, wise choices, and a little guidance and support can help you reach your financial goals.

“I can’t afford a house, so I might as well treat myself to a fun weekend.” That might seem like a good idea in the moment. But here’s the truth: small, intentional spending decisions can add up more quickly than you think, and help you reach big goals.

Reduced spending can also reduce waste in landfills. Ordering out for dinner means higher meal costs plus plastic bags, boxes and other disposable materials. Meal planning for the week on a free day helps you save money and reduce your carbon footprint.

Write down your financial goals

What are your financial goals? What’s important to you? SmartDollar, your no-cost confidential online personal finance program, is designed to help you reach your goals.

SmartDollar’s step-by-step plan helps you take small steps to pay off debt and save more using the online budgeting tool. It keeps you motivated with video lessons from personal finance experts and gives tips to:

Pay off debt faster

Set up an emergency fund

Save for college

Buy a car

Save for a down payment on a house

Free one-on-one financial coaching is also included. To sign up and get started, visit SmartDollar.com/enroll/costco or text Costco to 33789* to download the app.

If you want to grow your financial knowledge, additional financial resources are available through Resources for Living. Get a free 30-minute consultation per concern with a financial specialist. They can help with things like budgeting, credit repair and reports, mortgages and refinancing, debt management and tax questions. Visit RFL.com/Costco to request a free financial consultation.

Be smart about big purchases

Do your research before buying a house or car. Take the time to compare prices and learn about the market in your area. Consider things like rates and resale value to make an informed decision and get the best value for your money. Consider checking out the Costco Auto Program.

Watch these SmartDollar videos for additional ways to save:

Your Costco benefits can help you make the most of your money.

Save on monthly expenses — New for 2025, you have access to LifeMart for employee discounts on gym memberships, virtual fitness and childcare.**

Contribute to your 401(k) —Costco offers matching and annual contributions to your retirement plan with T. Rowe Price.To check your 40l(k) account balance, set up automatic payroll deductions, adjust your investment mix and much more, go to RPS.TRowePrice.com.

Purchase company stock — The Employee Stock Purchase Plan (ESPP) lets you buy Costco stock through payroll deductions. You choose the amount you’d like to invest per pay period. To learn more, visit Costcobenefits.com > Financial Wellbeing > Employee Stock Purchase Plan (ESPP).

Save on taxes — Use reimbursement accounts for eligible expenses.

A Health Care Reimbursement Account (HCRA) lets you set aside pretax dollars to pay eligible medical expenses. You can use it for things like copays, deductibles and coinsurance, dental and vision expenses, plus prescriptions and over-the-counter items. Sign up for an HRCA during Annual Enrollment. To learn more, visit Costcobenefits.com > Financial Wellbeing > Health Care Reimbursement Account.

A Dependent Care Assistance Plan (DCAP) lets you set aside pretax dollars to pay for qualified child and elder care expenses needed for you and your spouse to work. You can use it for expenses like day care, before- and after-school care, nursery and pre-school, and in-home aids. Keep in mind that the DCAP isn’tfor dependent health care expenses. You can sign up, change or stop your DCAP based on your dependent care needs. To learn more, visit Costcobenefits.com > Financial Wellbeing > Dependent Care Assistance Plan.

NOTE: If you were enrolled in a reimbursement account in 2024, remember that your claim filing deadline is April 30. Any unused funds are forfeited after this date. Only your HCRA rollover amount of up to $640 can be carried over from 2024 to use in 2025.

*Message and data rates may apply.

**Childcare discounts are not available in Puerto Rico.

Saving money not only feels good, it also gives you more control and opportunities throughout your life. With savings in the bank, you can more easily meet life goals, such as taking a big vacation, upgrading your home, or funding a child’s education.

And here’s the good news: Saving money is not as hard as it may seem. With some thought, planning and a little discipline, you can make small changes that can make a big difference.

Check out the ideas below for inspiration. And don’t forget to use your Costco benefits to help you reach your savings goals.

By setting up monthly automatic transfers from your checking account to your savings account, your money will build without any extra work on your part. Even if it’s just $25 a month, it will add up fast. Consider naming your savings account or accounts to match your savings dreams or goals, such as “vacation fund,” “emergency fund” or “down payment.”

Do take advantage of reimbursement accounts.*

Are your children in afterschool care? Do you need a dental crown replaced? Could your elderly parents use some in-home help? You can set aside pretax dollars for these expenses — and save money on taxes — with a reimbursement account administered by Inspira Financial (formerly PayFlex).

Enroll in a Health Care Reimbursement Account (HCRA) and/or a Dependent Care Assistance Plan (DCAP) during Annual Enrollment in November. You can also enroll in DCAP during the year if your childcare needs change.

Do teach your kids how money works.

Kids can and should develop good money habits at an early age. You can help by teaching them the connection between work and money and encouraging them to have short- and long-term savings goals. Younger children can watch their savings grow in a clear savings jar. Tweens and teens can be given more responsibility by using a banking app on their phone to follow their savings progress or make transfers from checking to savings.

Do start small.

It’s often easier to save if you start with a short-term goal. For example, committing to saving $20 a month for six months is more attainable than setting a goal to save $300 per month for a year. Once you reach your short-term goal, you’ll have created a habit of saving that can motivate you to keep going.

Don’t forget to monitor your autopay accounts.

Using autopay for gym memberships, streaming subscriptions and other services is a common practice. But this convenient way of paying also has its costs. In a recent survey, 42% of those polled continued to pay for subscriptions they no longer used.1 If you use autopay, make sure to regularly review what you’ve signed up for so you can cancel services you’re not using.

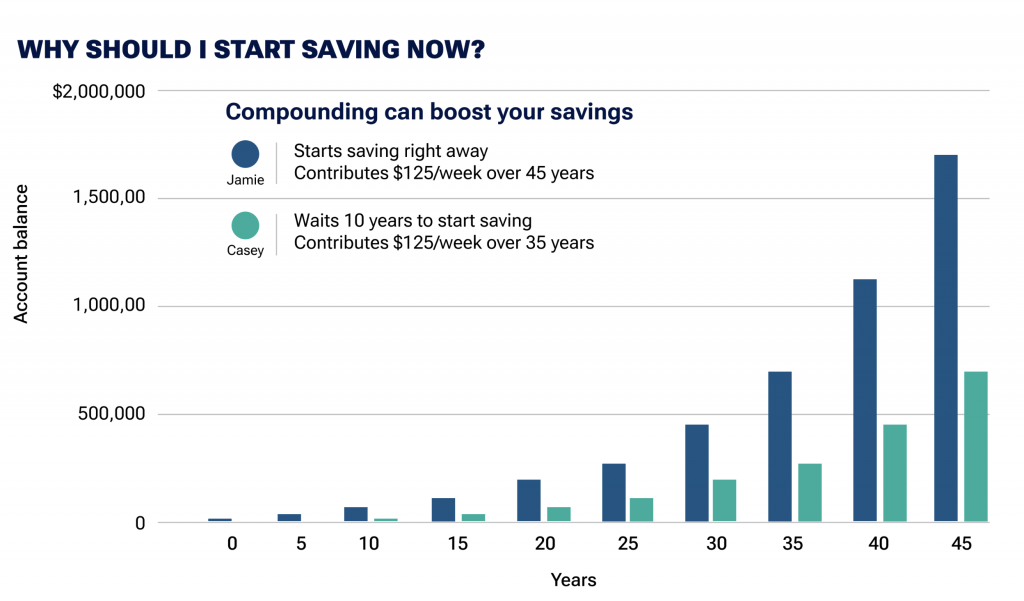

Don’t put off saving for your retirement.

Even saving a few dollars per paycheck for retirement can help you have a more secure financial future. The younger you start, the better, since you earn interest every year on both the money you save and the interest you earn along the way. For example, the chart below, provided by T. Rowe Price, shows the substantial impact that delaying your retirement contributions for ten years can have on the total amount you have available when you retire.

The chart is for illustrative purposes only and is not meant to represent the performance of any specific investment option. Final account balances are rounded to the nearest thousand. Assumes $125 invested each week in a tax-deferred account and a 7% annual rate of return for a hypothetical investor from age 20 to age 65. All investments involve risk, including possible loss of principal.

Costco’s retirement plan through T. RowePrice makes it easy to save with automatic enrollment. You can choose a percentage of your pre-tax income to contribute. Costco makes contributions to your retirement plan even if you don’t contribute yourself.

Don’t skimp on preventive care.

Medical and dental conditions have better outcomes — and are less expensive to treat — when detected early. Make sure to get your annual physical exams, dental cleanings, vaccines and recommended screenings. Preventive care is free when you use an in-network provider.

Don’t go it alone.

We all have something to learn about improving how we manage our money. A SmartDollar®financial coach meets you where you are financially to help you make the changes necessary to reach your savings goals. You can start these free one-on-one sessions at any time and sign up for as many as you want. Spanish-speaking coaches are also available.

Your financial well-being is unique to you. It’s based on how well you’re able to stay on top of your expenses, how secure you feel about your financial future and whether you have the freedom to make financial choices that allow you to enjoy life.

Breaking these goals down to small, manageable steps can help you take control of your finances. This month-by-month guide organizes these steps to make it easy to take action throughout the year. Bookmark this page so you can refer back and stay on track.

If you need help getting started, get free one-on-one financial coaching from SmartDollar®. Your coach can guide you through each step.

Create a budget. Use the EveryDollar budget app from SmartDollar® to simplify budgeting and help you track where your money is going.

Prepare for tax time. Gather last year’s forms and records, andsubmit your tax return as soon as you’re ready but no later than April 15, 2024.

April: Work on your money management

Start or fully fund your emergency account. Aim to save $1,000, then build your account to cover three to six months of expenses. Use your tax refund to replenish your account.

Automatedeposits. Set up recurring contributions to your savings account or investment account.

May: Improve your financial standing

Check your credit report. Request this free summary of your credit history from a credit bureau, such as Experian or Equifax, and check for errors.

Review your debt. Consider following the debt snowball method from SmartDollar.

June: Do a mid-year checkup

Check your budget. Are you sticking to it? If priorities have shifted, adjust accordingly.

Review your investments. The mix of stocks and bonds in your investment fundsshould match your tolerance for risk and length from retirement.

July: Invest in yourself

Practice mindful spending.Waiting a pre-set period (such as 30 days) before you buy will help make sure you really want a particular big–ticket item.

Educate yourself. Find a podcast, book or blog to learn more about financial topics that interest you.

August: Focus on your or your children’sfuture

Identify and save for your goal. Are you planning to buy a home, travel, or retire at 55? Set money aside each month (automatically through your bank, if possible) to fund your goal.

Open a 529 account. These investment accounts can help you save for your child’s college, graduate school or vocational training.

September:Stay safe online

Protect your passwords. The strongest passwords include upper- and lowercase letters, numbers and symbols, and made-up words that don’t appear in the dictionary.

Watch for fraudsters.Don’topen or reply to unsolicited emails asking for financial information, and if the URL looks strange in any way, don’t respond.

October: Give back

Donate.Costco’s Workplace Giving Campaign starts this month. Every contribution you make supports the local community and is matched by Costco at 60%.Watch for the notification email.

Volunteer. Donating your time and energy is just as valuable as giving money. Look to your local food banks, schools, nursing homes, and other community resources for opportunities to volunteer.

November:Understand your options

Evaluate your insurance.Review your coverage during Annual Enrollment. Get familiar withyour voluntary short–term disability options, and your basic life, basic accidental death and dismemberment (AD&D), and long-term disability insurance covered by Costco.

Update your estate plan. Review and update beneficiary designations. Create or update your will with help from Resources For Living.

December: Prioritize your retirement

Fund your future. Aim to increase your retirement contribution next year. Costco helps you save for your retirement by automatically increasing your contribution annually.

According to Scientific American, “Joint disorders and low back pain consistently rate among the most common reasons U.S. adults visit their doctors.”1 Although physical therapy is an effective treatment for these conditions, many patients have difficulty getting the care they need.

The cost and inconvenience of multiple appointments over weeks and months can make in-office physical therapy challenging for people seeking treatment. So what’s the solution? Virtual physical therapy.

Not only is virtual physical therapy convenient. It’s a bargain for patients. You can save time, money on gas and parking and the cost of your care. There’s even better news for Costco employees. You and your family members (age 13+) who are enrolled in a Costco medical plan can get virtual physical therapy at no cost through Omada for Joint & Muscle Health.

In a pioneering study, researchers at Duke Clinical Research Institute used virtual therapy with 143 patients who underwent total knee replacement at four different providers. A second group of 144 patients was prescribed traditional physical therapy.

The researchers found an average cost savings of $2,745 per patient treated using virtual physical therapy.*

Janet Bettger, Ph.D., associate professor with the Duke Department of Orthopedic Surgery and the study’s lead author, said the patient experience was also positive. Study participants who underwent a second knee replacement and who had virtual physical therapy the first time requested virtual physical therapy on their second surgery, she said.2

Virtual therapy with Omada for Joint & Muscle Health

If you’re recovering from an injury, virtual physical therapy with Omada for Joint & Muscle Health could be right for you.

Here’s how it works:

Visit Omada Joint & Muscle Health on your phone or other digital device. Click “Apply today,” complete the application, then click on “Treating pain and injury,” and enroll. Within 48 hours, you’ll receive a call from your licensed physical therapist. You’ll have the same dedicated physical therapist throughout your treatment.

Your physical therapist will carefully assess your condition by guiding you through a series of movements and performing a full musculoskeletal evaluation.**

They’ll recommend your best care option — whether you choose Omada’s virtual physical therapy or prefer to see a local, in-person physical therapist.

Your virtual physical therapist will partner with you to provide:

A personalized recovery plan designed to treat the source of your pain

App-guided exercises with 3D animations and voice narration to ensure proper pacing and form

Step-by-step guidance with support, adjustments, education and more

An exercise kit, complete with elastic bands, door anchor and a phone stand

Concerned about preventing injury?

Omada also offers an injury prevention program for people who want to avoid joint or muscle pain in the future. Whether you’re starting new work responsibilities, taking up a new sport or just looking for an overall physical tune-up, it’s easy for your body to get out of balance. This program can be tailored to your changing needs, helping you focus on your flexibility and strength so you can guard against future pain and injury.

*Outcomes and costs were measured three months after the procedure, according to the study.

**This evaluation will not satisfy the requirement for spine surgery pre-authorization. This type of surgery generally requires the following: In-person physical therapy for at least 6 weeks within the last 12 months. Your plan offers access to an expert second opinion by 2nd.MD. If you would like to call them the contact number is 833-579-2509.

1Scientific American. Virtual physical therapy could help fill gaps in treating all too real pain.

You teach your children about safety, physical health, good study and work habits, acceptable behavior, and more. You want to instill in them all the things they’ll need to function well once they leave the family nest.

So why not include lessons on how to earn and manage money? After all, it makes sense for everyone to learn to spend wisely, save and invest what they earn.

The best way to start teaching your children about money is to show them how you handle it. As soon as your children are old enough to understand, include them in your family’s budgeting, planning and saving discussions. As a bonus, your kids will know what to expect in terms of what the family can afford. They’ll also learn how their own choices can help them get things they want.

Be a role model for your children

Make sure your own financial behavior is responsible. If they see you spending money on things you don’t need instead of paying your bills, they may grow up thinking that’s an acceptable way to handle finances.

If you use credit cards, make sure your kids also see you checking your credit card statements and paying your bills on time. Show your children that those little plastic cards aren’t magical sources of free money. Let them see how much interest you pay, too.

Help them practice decision-making

Let your children manage their own funds. When they get old enough, help them open and maintain a bank account. Whether they earn an allowance or income from a part-time job, help your kids make good decisions with their funds.

A lesson about saving on taxes

As every grown-up knows, taxes can be complicated. But it’s never too early to teach your children an important lesson: it pays to take advantage of the tax benefits you have.

For example, with a reimbursement account, administered by PayFlex®*, you can set aside pretax dollars and pay yourself back through a Health Care Reimbursement Account or a Dependent Care Assistance Plan.

The Health Care Reimbursement Account (HCRA) allows you to reimburse yourself for health care costs your medical plan doesn’t cover, such as out-of-pocket costs for medications and copays. The Dependent Care Assistance Plan (DCAP) lets you set aside pretax dollars to reimburse yourself for eligible child (under age 13) and elder care expenses necessary for you and your spouse to work, including child care and nursery/preschool costs.

Talk to your kids about how these accounts help your family save money on taxes. And remember to enroll in an HCRA or DCAP during Annual Enrollment.

*Available in Mainland and Hawaii.

Give your kids the tools to succeed

Encourage your children to save, and guide them in setting up a personal budget. Teach them how to compare prices before buying a pair of sunglasses, a skateboard or something else they want. Show them how much an investment account can grow over time by reviewing your retirement account’s growth together. That way, they can see the importance of saving even a small amount as soon as they start working as adults.

If they make a money mistake, don’t be too quick to bail them out. Instead, help them learn from it so they’ll make a better decision next time. As they get older, you can even show them more details about your family’s finances. For example, you can explain how interest can add up when you don’t pay off your credit cards each month or why making dinner is easier on your budget than ordering take-out.

Your kids can learn from all sorts of activities, including:

Counting the coins in a piggy bank

Creating a budget on paper or online

Checking monthly statements for charges for apps and subscriptions

Buying a used car and shopping for insurance

Opening a savings account

Researching how to finance their education

You can find teachable moments just about every day. It’s never too early to start setting your children up for financial success.

It’s great to have money, but who wants to think about it? The short answer is: You do. Because the earlier you think about it, the better. If you’ve decided it’s time to learn more about money and get your financial life on track, congratulations. Getting control of your finances is the first step toward achieving the financial life you’ve always wanted.

If you’ve already decided to learn about money and create a financial plan, you’re one step ahead of most people. An important next step can be to share your journey with friends and family. That way, when they check back with you about your progress, you can be accountable to someone. Remember: Goals that aren’t written down are just wishes. So write your decision down, share it with loved ones and stay accountable.

After making your decision, you’ll want to know exactly where you stand. One way to do that is to look at your credit report so you know what information lenders are seeing about you. Check with any of the three credit score issuers: Transunion®, Equifax® and Experian®. Review your credit report carefully and be sure to challenge any mistakes or inaccuracies.

Make a plan — and a budget

Looking through your credit report can give you an idea of the existing debt and expenses you have. Write down all your monthly expenses and your monthly income. Capturing your total income and expenses is the first step in making a budget. Depending on your history with money, you may have a negative association with the word budget, but it’s important to remember that a budget is just a tool. It can help you stop spending money on things that aren’t important to you, so that you still have money to spend on the things that are important to you.

Cut your expenses

Again, you’ll want to make sure your budget is written down and tracked. Once you’ve been budgeting for a few months, you’ll start to notice patterns in where and how you spend your money. Decide which expenses align with what’s important to you, and cut the things that don’t. Use any extra money each month to create an emergency fund and reduce your debt.

Grow your income

While many budgeting guides talk about eliminating that daily coffee purchase or unused gym membership, that’s only one side of the story. There’s only so much you can cut out of your budget, while in theory at least, you have unlimited income potential. Look for more ways to save in your spending when you go shopping, or out to dinner. Wait for larger items to go on sale before you pay the full price. And also look for ways to bump up your income — perhaps selling items you don’t need or doing small jobs in your spare time.

It’s a marathon — not a sprint

Finally, remember that financial health is a marathon, not a sprint. Depending on where you’re starting, you may not completely eliminate your debt in a few months or even a few years. It will take time. So it’s important to remember to be steady and patient. And not all months will be the same. There will be times when you slip up and make poor financial choices. This is another reason why writing down and tracking your progress can be useful. It helps you see that if you have a bad financial day, you’ve also had many good days. You’ll get there.

Need help?

As a Costco employee, you have access to SmartDollar®, a financial well-being program, as well as one-on-one financial coaching, that’s included in your Costco benefits — at no cost to you. In addition to educational content from financial experts, it offers a full suite of budgeting, tracking and financial tools, plus Dave Ramsey’s 7 Baby Steps program. This proven program is designed to help you learn how to stick to a budget, get out of debt, save for the future and retire with confidence — no matter where you start.

The bottom line

Deciding to manage your financial situation, track your expenses, learn to budget and get control of your money is one of the best financial decisions you can make. Building on a sound financial foundation can provide peace of mind and help you lead a more stable life. Decide to start, write it down and share it with trusted friends and family. Gather information on your monthly income and expenses and start a budget.

Remember, sharing your decision and your progress with others helps keep you accountable, even when the inevitable slip-ups happen. When you do slip up and make a poor financial decision, the most important thing you can do is acknowledge that it happened and plan to do better tomorrow. One day at a time, you’ll find your path to a brighter financial future.

Source:Intuit MintLife. Getting my finances together: Where do I even start?

*With more than 90 days of service.

If you’re ready to live your best financial life, the following resources can provide the support you need.

Is your credit card debt keeping you up at night? Are you putting money into a retirement plan? Is your dream vacation just that — a dream? Is buying a house out of the question? Maybe now is the perfect time to stop worrying about money and start taking control of it.

As this informative three-minute video suggests, you can learn how to set reasonable financial goals and accomplish them.

e-Health video: Setting financial goals you can reach

It’s true that money doesn’t buy happiness. But having a healthy relationship with money can help you feel more secure and less stressed. Setting and working toward financial goals can help you maintain that healthy relationship.

Goals everyone should have

Some financial goals can help everyone, no matter what their income level, family situation or favorite hobbies happen to be. Spending less than you make would be one of those goals.

How to spend less than you make

Track your take-home income and expenses. Be sure to include any annual expenses — divide them by 12 for a monthly budget — and add in your best estimate for unknown costs, such as car repairs or health insurance deductibles and copays.

If you’re spending more than you make, you may find yourself a little (or a lot!) deeper in debt from year to year. That means you’ll also pay more in interest. There are three ways to help you start or continue to spend less than you make:

Earn more. Sell stuff – try a yard sale or selling items online. Volunteer to work overtime if you’re able to. Try freelance work or a side job.

Spend less. That’s where tracking your spending makes a difference. Even if you’re making good progress toward your saving goals, see where you can cut back. You may be able to reach your goals even faster than you think.

Do both! Many people, when they earn more, start spending more. Try doing the opposite. Next time you get a raise, save more and spend less. It’ll help you reach your financial goals.

Goals unique to you

Your financial goals can be anything, but many involve saving up for things, like:

A down payment on a house, a car or even just a new toaster oven

Experiences, like vacations and other fun activities

Educational opportunities for yourself or family members

An emergency fund, or

Retirement

Many banks let you divide your savings account into separate “buckets” so you can allocate funds toward different goals. And for some large goals, such as college and retirement, it makes sense to research investment accounts and learn about the risks and possible rewards.

Reaching your goals can take time and discipline. The steps themselves are simple, yet some people find them difficult to follow. Above all, be sure to:

Spend less than you earn, and

Put money aside toward your goals each time you get paid

You can even set up your payroll or bank accounts to transfer funds automatically. It can help to keep your checking account for paying bills separate. That way, you’ll be less likely to spend your goal-reaching funds without realizing it.

Try these simple steps to help reach your financial goals.

Resources For Living®

The EAP is administered by Resources For Living, LLC. This material is for informational purposes only. This material provides a general overview of the topic. Information is not a substitute for professional financial or legal advice and is not meant to replace the advice of tax or financial advisors, legal or other professionals. Information is believed to be accurate as of the production date; however, it is subject to change.

How do you get out of debt, stretch your paycheck, grow your savings, and prepare for retirement and other big-ticket life expenses? The smartest move you can make is to get started now with some practical guidelines from this short video.

When it comes to financial stability, the earlier you get there, the better off you’ll be in the long run. But you won’t have to do it alone. Your Costco benefits can help. They offer information that can help you develop healthy financial habits and ways to help you build your nest egg. For more information, check out the “Resources for you” section below.

Source:Healthwise. 5 ways to create financial stability.

Have you always wanted to get your degree? Would vocational training prepare you for work you’ve always wanted to do? Are you hoping to send your kids to college?

According to U.S. News & World Report, the average cost of tuition and fees for the 2022–2023 school year is $39,723 at private colleges, $22,953 for out-of-state students at public colleges and $10,423 for in-state residents at public colleges.1 But financial help is available. Get started by taking the five steps below.

First, try to get “free” financial aid (the kind you don’t have to repay). Scholarships are an attractive type of aid because they do not have to be repaid and many are not based on financial need. They may be awarded to students who have excelled in specific academic areas, or specialty areas such as music or sports. Thousands of private scholarships are available through various companies, organizations, private foundations and clubs. Information may be found online at numerous sites, including fastweb.com or Scholarships.com. Comprehensive guides are published and updated each year on specific scholarships, eligibility criteria, etc., such as the College Board Scholarship Handbook or Peterson’s Scholarships, Grants and Prizes.

Costco is making college more affordable for employees

The Costco Employee Scholarship is available in amounts up to $2,500 per academic year for up to four years for eligible Costco employees.

To be considered for the Costco Employee Scholarship, applicants must:

Be a regular part-time or full-time Costco Wholesale Employee residing in the United States (College Retention employees are eligible to apply).

Be enrolled or planning to enroll in an accredited U.S. college or university.

Have a high school diploma or equivalent by June 2023.

Plan to pursue a 2-year or 4-year undergraduate degree or certificate at a nonprofit, accredited college or university in the United States starting fall 2024

Not have obtained a bachelor’s degree at this time.

Learn more about the Costco Employee Scholarship, including the application timeline. To check your eligibility, call 877-655-4097.

Free financial aid usually doesn’t cover 100% of your costs. So you may need to find other ways to pay for college or vocational school, including taking out low-cost loans and using any money you may have saved.

To apply for any financial aid, you’ll need to complete the FAFSA® form. This is the financial aid application used by the federal government and most colleges and universities. If you list more than one college on your FAFSA, you’ll receive a financial aid offer from each of those schools. These offers will likely contain a combination of free aid and low-cost loans. Review each school’s financial aid offer carefully.

Step 2: Know your deadlines.

Financial aid deadlines are specific to your situation — your school, where you live, what you study.

The FAFSA deadline is the most important deadline you should know. Check the FAFSA deadlines.

Deadlines for aid from your state, school and private sources tend to be earlier than those for federal aid.

Make sure you have some way to keep track of all your deadlines. For example, write important dates on a calendar, or track them on your smartphone.

Step 3: Fill out the FAFSA.

You must complete the FAFSA every year to qualify for:

Federal and most state grants, scholarships, low-cost student loans, and work-study programs

State programs

Many school-based financial aid programs

The FAFSA is your ticket to financial aid. Check the FAFSA deadlines.

Step 4: Compare schools’ financial aid offers carefully.

How schools determine your financial aid

The schools that you list on your FAFSA receive a Student Aid Report (SAR), which details your FAFSA results. The SAR reports your expected family contribution (EFC).

Here’s how it works:

Each school uses your EFC to calculate your financial need. This determines your eligibility for financial aid.

Then each school creates your financial aid offer, which can contain federal, state and institutional grants, scholarships, work-study, low-cost loans, and other aid.

Understand what you have received.

Your financial aid offers will differ from school to school. This is based on differences in the cost of attendance, available aid and school-specific criteria for awarding certain types of aid.

When comparing your financial aid offers, consider the following:

Calculate the percentage of the offer that is “free” money. You don’t have to repay free money if you continue to meet all the obligations. So the more free money you get, the better.

Compare “apples to apples” when it comes to the actual cost of attending each school. The actual cost encompasses more than just tuition; it includes books, meals, housing and more.

Make sure you understand the long-term responsibilities associated with each financial aid offer, and choose the most appropriate offer for your situation:

Does your financial aid offer contain any grants that may become loans and require repayment?

Will you or your child have time for a work-study job?

Are you or your child prepared to pay back any educational loans?

Step 5: Be sure you have the money you need.

Once you’ve received your financial aid award, you need to make sure you have enough money to cover all your education costs.

Know your education costs

Direct costs — Costs associated with attending school that are included in your award letter:

Tuition/fees

Room/board (institutionally owned housing)

Meal plan

Books and supplies

Miscellaneous personal expenses, as determined by the school

Parking

Transportation

Indirect costs — Additional costs that may require money beyond what’s allotted in your award letter:

Off-campus housing

Food not purchased through a meal plan

Medical coverage

Be smart about borrowing

What should you do if you have exhausted all sources of funding, including scholarships, grants and low-cost federal loans, and you still have college costs to cover? First, contact your school’s financial aid office. Your school may offer payment plans that let you distribute your payments throughout the year.

Consider private education loans only as a last resort. Private education loans often have higher interest rates, more fees and less flexible repayment options than federal loans do.

Be sure you have exhausted all other financial aid options before applying for a private education loan.

Borrow only what you need to cover your costs, not what you are eligible to receive.

Understand the terms of the loan before you agree to (and sign) anything.

Find out if you can defer payments while in school or get a lower interest rate with a co-signer.

*Resources For Living is available to all employees and members of their household, including children up to age 26 living away from home.

If you or a member of your household is interested in pursuing a college education or vocational training, the following resources can help you discover ways to pay for it. These resources are confidential and available to you at no extra cost.